The OECD's latest forecasts (p.236) suggest that the UK is now slipping back into recession, with negative quarter-on-quarter growth in the fourth quarter of this year and the first quarter of 2012. This is in line with my own forecasts, though the OECD predicts a somewhat earlier recovery - with second quarter output rising, and (very) modest growth (but growth nevertheless) of 0.5% in 2012, taking the year as a whole.

The OECD also expects (p.222) the output gap - the gap between actual and potential output - to rise during 2012; this is a predictable consequence of recession. In the wake of the severe fall in output during the Great Recession, their estimates of the magnitude of this gap still look to be on the low side.

The forecasts for unemployment, unsurprisingly given renewed recession and very feeble recovery, are for continued increases over the next two years.

Sunday, November 27, 2011

Details of the government's credit easing scheme have started to emerge in advance of this week's Autumn Statement. The government will introduce three schemes aimed at increasing the flow of credit to firms. These include underwriting bank loans, putting government money into an investment fund run jointly with the private sector, and enabling companies to issue bonds directly to the market. Together, these schemes should provide a significant flow of funds to businesses just at a time when conditions in the financial sector appear once again to be tightening. The package is very much to be welcomed.

Meanwhile, the Office for Budgetary Responsibility looks set to reduce its growth forecasts. This is no surprise - as I have stated elsewhere on this blog, a reasonable forecast for the coming months is for renewed recession. The credit easing package will not prevent this - the buffeting that demand is taking from the downturn in our major trading partners is too severe to be fully mitigated by any plausible dometic policy - but it will, to some extent, help.

Meanwhile, the Office for Budgetary Responsibility looks set to reduce its growth forecasts. This is no surprise - as I have stated elsewhere on this blog, a reasonable forecast for the coming months is for renewed recession. The credit easing package will not prevent this - the buffeting that demand is taking from the downturn in our major trading partners is too severe to be fully mitigated by any plausible dometic policy - but it will, to some extent, help.

Friday, November 25, 2011

John Muellbauer reminds us of Wim Boonstra's proposal for conditional Eurobonds - these would allow indebted economies to borrow on the financial markets at a rate of interest which - if conditions on their success in tackling their indebtedness are met - is contracted to fall over time. Boonstra first proposed such an instrument in 1991 - long before the introduction of the Euro. It's a clever idea.

Whether conditional bonds alone provide a solution to the current crisis is moot, however. The high interest rate premia (over and above German rates) that attach to Italian bonds - the spread is still around 5 percentage points. The corresponding measure for Spain is almost as high. The measures for Greece and Portugal are in silly territory. One might argue that the European Central Bank (ECB) needs to inflate some of the debt away in order to make conditions right for the introduction of conditional bonds. But if, by putting such bonds in place, we could guarantee that such an inflation would be a one-shot event, convincing the (still inflation-shy) German government that this is what the ECB must do might become a more feasible proposition.

Wim Boonstra (1991). The EMU and national autonomy on budget issues: an alternative to the Delors and free market approaches Finance and the international economy: the AMEX Bank Review prize essays, 4

Whether conditional bonds alone provide a solution to the current crisis is moot, however. The high interest rate premia (over and above German rates) that attach to Italian bonds - the spread is still around 5 percentage points. The corresponding measure for Spain is almost as high. The measures for Greece and Portugal are in silly territory. One might argue that the European Central Bank (ECB) needs to inflate some of the debt away in order to make conditions right for the introduction of conditional bonds. But if, by putting such bonds in place, we could guarantee that such an inflation would be a one-shot event, convincing the (still inflation-shy) German government that this is what the ECB must do might become a more feasible proposition.

Wim Boonstra (1991). The EMU and national autonomy on budget issues: an alternative to the Delors and free market approaches Finance and the international economy: the AMEX Bank Review prize essays, 4

Thursday, November 17, 2011

The Nationwide's consumer confidence index took another tumble in October. The index has now fallen to a level below the previous worst ever scores (observed in January 2009 and February 2011). The economic environment is turbulent and the gloom is justified. Much of the policy response has now to come from abroad, with the EU still struggling to establish a coherent approach to the debt problem. But we must also look to the Chancellor's Autumn Statement at the end of this month to provide a boost to demand.

Monday, November 14, 2011

The latest forecasts from my neural network model, based on industrial production data for the UK, continue to indicate a serious slowdown in activity in the current quarter. The model expects the contraction to gather pace until the end of next summer, and growth to resume only in mid-2013.

I first reported the dip expected for the last quarter of 2011 on this blog as long ago as June 2010.

I first reported the dip expected for the last quarter of 2011 on this blog as long ago as June 2010.

Tuesday, November 08, 2011

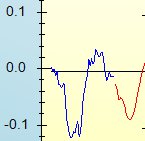

The divergence between the 3 month London Interbank Offered Rate (LIBOR) and the interest rate set by the Bank of England's Monetary Policy Committee was often, during the immediate aftermath of the 2008 credit crunch, cited as evidence that the banking system was not working as it should. In normal times, LIBOR is close to - typically a tenth or two-tenths of a percentage point above - the Bank of England's rate. Following the cut in the Bank's rate to 0.5%, the gap between the two rates fell back to near normal magnitudes. But it has been rising throughout this year. In January, it stood at 0.76% - some 0.26 percentage points above the Bank of England's rate. Today it has risen to 1%, and the rate at which it is increasing has been growing over recent months. The illness afflicting the banking sector may have gone into remission for a while - but the sickness is back.

One bank's reluctance to lend to another reflects a lack of confidence by the former bank in the latter - and across the system it suggests that bankers are becoming increasingly cautious. This has an adverse effect on the real economy as businesses and households find it harder to gain access to loans. At a time when growth is faltering, a second petrification of the financial sector represents really bad news.

And, as an article in last Tuesday's Wall Street Journal argues, the gap between base rates and LIBOR is now probably understating the extent to which financing has become difficult.

One bank's reluctance to lend to another reflects a lack of confidence by the former bank in the latter - and across the system it suggests that bankers are becoming increasingly cautious. This has an adverse effect on the real economy as businesses and households find it harder to gain access to loans. At a time when growth is faltering, a second petrification of the financial sector represents really bad news.

And, as an article in last Tuesday's Wall Street Journal argues, the gap between base rates and LIBOR is now probably understating the extent to which financing has become difficult.

Tuesday, November 01, 2011

The UK economy grew by 0.5% in the third quarter of this year. This is faster than had been expected by many observers - myself included. It has to be regarded as welcome news.

But the outlook for the current quarter and the immediate future remains challenging. World demand remains muted, and the fiscal policy stance within the UK does little to promote growth. On the monetary side, interest rates remain low and the quantitative easing programme has restarted - these policies have moderated the adverse impact of other things, but it is not clear that they alone will be sufficient to underpin continued growth over the coming months.

The Chancellor of the Exchequer will make his autumn statement on 29 November. This may need to offer some fiscal easing if the relatively good outcome of the third quarter is to be sustained.

But the outlook for the current quarter and the immediate future remains challenging. World demand remains muted, and the fiscal policy stance within the UK does little to promote growth. On the monetary side, interest rates remain low and the quantitative easing programme has restarted - these policies have moderated the adverse impact of other things, but it is not clear that they alone will be sufficient to underpin continued growth over the coming months.

The Chancellor of the Exchequer will make his autumn statement on 29 November. This may need to offer some fiscal easing if the relatively good outcome of the third quarter is to be sustained.

Subscribe to:

Posts (Atom)